Paths leading to strengthening

your company’s net worth.

Código Líder Fiscal is a company with technology that aims to provide fiscal and tax solutions for the business market.

Jean Carlo de Sene Sousa - CEO Código Líder Fiscal

Código Líder Fiscal is a company with technology that aims to provide fiscal and tax solutions for the business market.

Jean Carlo de Sene Sousa - CEO Código Líder Fiscal

Solutions based on parameterization in the rules contained in all current legal systems.

With a team of specialists in the tax, legal, tax and accounting segment, Código Líder brings solutions and assertiveness in its work.

Through powerful software we present solutions with analysis and notes of taxes unduly paid.

We are a company with TECHNOLOGY that aims to provide TAX and TAX solutions for the business market. Our aim is to present to YOU ENTREPRENEUR and to YOUR TEAM of specialists in the tax, fiscal or accounting segment, some of our solutions that can contribute to your routine with speed and assertiveness, in the validations, processing and crossing of data and information.

Código Líder Fiscal

Check out the video Léo Chaves explaining how to reduce your company's tax burden.

Código Líder Fiscal

Check out a little about the Código Líder Fiscal and our services in the video.

All solutions are developed and parameterized based on the rules contained in the current legal system. Our aim is to present YOU BUSINESSMAN AND YOUR TEAM of specialists in the tax, fiscal or accounting segment, some of our solutions that can contribute to your routine with speed and assertiveness, in the validations, processing and crossing of data and information.

Stay on top of market news in the tax, fiscal or accounting segment and the benefits they can bring to your company.

© Copyright 2021 - Código Líder Fiscal - All rights reserved. ![]()

The collection of PIS and Cofins taxes is mandatory and must be done by all companies, whether under the cumulative regime or non-cumulative.

In the case of those opting for the Simples Nacional, there is the opportunity to identify whether the revenues from single-phase products have been taxed against PIS and COFINS in the last 5 years.

These are monophasic products, pre-established by laws, such as, for example, personal hygiene, highlighted in Law 10.147/2000. To avoid overpayments and, consequently, save significant amounts, companies must pay attention to tax planning and rely on professional guidance.

The single-phase incidence is intended to allow the collection of contributions once within the circulation chains of goods or services. That is, giving the importer or manufacturer of the goods the responsibility for the taxes of the entire production chain. It is a regime that allows the reseller, wholesaler and retailer not to pay these taxes.

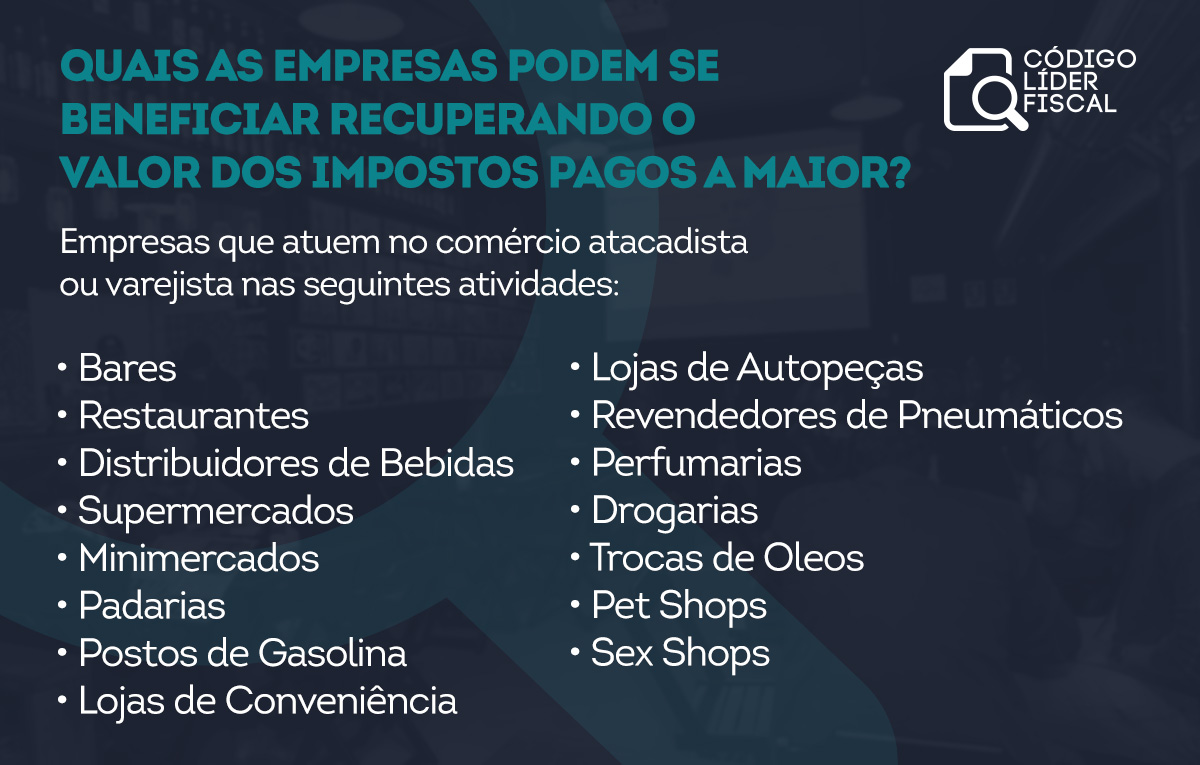

Only goods pre-established by legislation can have PIS and Cofins collection under the single-phase regime. These include: beverages, pharmaceuticals, personal care products, fuels, cooking gas and vehicle parts.“Any companies that participate in this distribution chain can benefit from this legislation and be free from paying these taxes. It is important to highlight some that are directly impacted, such as: auto parts, sex shops, pharmacies, supermarkets, bars, restaurants”, completes the CEO of the Tax Leader Code, Jean Carlo Sene.

This model allows for the reduction of tax evasion cases and the increase of impartiality in the Brazilian tax system.“It's a regime very similar to the tax substitution regime and, like all tax planning, it demands a lot of attention from the entrepreneur. So, to avoid double payment, the revenues from the sale of the products mentioned must be separated to indicate the single-phase incidence, that is, concentrated taxation” , explains CEO Jean Carlo.

Also according to the CEO, for taxpayers who paid the highest amount of taxes, it is necessary to search for compensation/refund of amounts.“The recovery of unduly paid taxes is a right of the entrepreneur. It must be carried out in stages established by the Internal Revenue Service, so it is interesting for the taxpayer to count on the help of a company specialized in this accounting, both for the correct return of the amounts and to avoid errors that could result in tax evasion" he points out.

About the Simple National

The Simples Nacional (SN) is provided for in Complementary Law No. 123, of 2006. It is a system that simplifies the payment of taxes for companies with annual gross revenue of up to R$4.8 million. Before this legislation, small businesses paid federal, state and municipal taxes, through separate guides, without distinction from large corporations. With SN, payment is made in a single tab, called DAS.

The Internal Revenue Service provides a model for offsetting taxes that are overpaid in a retroactive period of five years. Therefore, the help of a professional is essential for the entrepreneur to be able to carry out this accounting. With the technologies that the Tax Leader Code has, for example, it is possible to fully identify these single-phase revenues and also obtain a refund in the checking account within 60 days”, he concludes.

Brazilian tax issues are broad and are in constant change and adaptation. Taxpayers are affected daily by changes in laws, decrees, regulations, among other texts, which define the more than 90 existing taxes. Complying with these standards is a challenge, both to avoid default and to pay undue taxes or overpayments for the enterprise. For greater security and tranquility for businessmen, the Tax Leader Code offers a free tax diagnosis, with the possibility of anticipating risks and problems with regulatory bodies.

The market is competitive and demands from the company greater agility in carrying out operations and reducing costs."The taxpayer must always keep in mind that tax planning is the best tool that the company can count on is what enables the profitability and survival of the business, so this activity cannot be implemented last, let alone be done in the long term . And this is the main point for the entrepreneur to look for a tax consultancy company: to obtain solutions quickly and, above all, safely”, points out the CEO of the Tax Leader Code, Jean Carlo Sene

Code Leader Fiscal is a national company, headquartered in Belo Horizonte (MG) and with offices in four other states in Brazil, namely: Bahia, Distrito Federal, Rio de Janeiro and São Paulo. It uses artificial intelligence and proprietary technology capable of reading 60,000 lines per second to assertively identify the amount a taxpayer is entitled to recover from overpaid or improperly paid taxes in the last 5 years. “We are currently the only company in Brazil that provides entrepreneurs with a thorough analysis of 100% of the items recorded in Speds and Purchase and Sale Invoices, with precision, speed and depth. With unique work and safe for taxpayers, we issue reports in less than a month to be used immediately with the crossings considered liquid and certain”, continues Jean Carlo.

With an interdisciplinary team specialized in accounting for contracted tax reviews, the Tax Leader Code operates based on current legislation and supplementary normative instructions.“The taxpayer is pressured all the time by Organs regulatory bodies and this makes the company's tax management difficult. We make a commitment to the client for tax and legal support at all stages. We streamline the processes and, after analyzing the documents provided by the taxpayer, we generate cash flow for the company in about two months”, he adds.

Among the works carried out by the Tax Leader Code are: exclusion of ICMS from the PIS and Cofins basis; credits not recorded and not used in the law of non-cumulativeness of these contributions; exclusion of indemnity funds from the INSS tax base; rectification of SEFIP with the new GFIP; retention of 11%; unconstitutionality of the 10% FGTS fine; calculation of accumulated ICMS/SP credits, Reimbursement of ICMS-ST, TUST TUSD, exclusion of ISS from the PIS and COFINS calculation base, exclusion of PIS and COFINS from the base itself, Exclusion of fees from credit card and card companies of debts from the PIS and COFINS calculation bases and, even, of simple national companies, we promote the refund of taxes paid on single-phase or ST products,“We always recommend the Tax Tax Review for companies in Brazil, either by administrative or judicial measures, since the Tax Leader Code is remunerated only when, and if, there is success in the economic benefit, that is, zero cost and risk for the entrepreneur, who has nothing to gain", he concludes. Jean-Carlo.

Brazilian tax legislation is constantly changing and has numerous rules that can cause confusion and make entrepreneurs pay more than they really need. Considering this reality, the Tax Leader Code proposes specific tax solutions for the most varied businesses, including Social Security Compliance, which aims to identify whether your company has paid the highest INSS in the last 5 years and thus recover all amounts improperly collected by taxpayers.

Social security compliance provides the issuance of a precise diagnosis that helps reduce costs and recover amounts paid unduly. All this, with the implementation of careful analysis of all actions and operations carried out by the company. Four main themes are worked on for the application of this technique: indemnity funds, SEFIP/GFIP rectification, RAT/FAP reclassification and 11% retention”.

The indemnity amounts consist of the recovery of credits of amounts paid unduly referring to the non-levy of the INSS. The indemnity labor amounts may be excluded, such as: indemnified prior notice, 15 days of medical accident or serious illness, 1/3 vacation, food voucher, daily allowance, transportation voucher, education allowance, among others, some must be discussed in court while others can be recovered administratively. Therefore, it should be clear to the taxpayer that there will be an incidence related to amounts of a remuneration nature."To provide more security in refunds like this, we work with conservative standards and highlight the funds that are defined and judged by the Supreme Court and that can be administratively refunded through compensation and the others we discuss in court and await the final judgment. ”, explains the CEO of the Tax Leader Code, Jean Carlo Sene.

The SEFIP rectification, in Jean Carlo Sene's opinion, “is the only way to characterize the tax credit, or overpaid tax, and at this point is the main differential of the Codigo Lider Fiscal, which does this automatically, or rather, through technology, as it is useless to identify that there was an incidence of INSS in the indemnity amounts if you do not rectify the SEFIP, because if you do not generate a new GFIP, proving that it was overpaid, there is no credit"

Mainly with version 8.0 implemented, as of it, the GFIP/SEFIP rectification starts to be carried out in the SEFIP application with the issuance of the “Proof of Declaration to Social Security”. The new form of delivery replaces the previous information in the Social Security Register for the same key and allows the correction, when necessary, of the FGTS data. It is applied to any competence equal to or greater than 01/1999, even if generated in a version equal to or prior to 7.0. For this accounting data and information from payrolls, SEFIPs files and generation of rectified files of this system are used.

The Social Security Accident Fact (FAP) and the Environmental Work Risk (RAT) were instituted to minimize the percentage of work accidents in a company and, consequently, reduce the expenses generated for Social Security. The company's performance is attributed by the FAP result, a multiplier that can vary from 0.5000 to 2.0000. These values are applied, to four decimal places, on the RAT rate, being 1% if the activity is of minimum risk, 2% medium and 3% in cases of severe risk. “The entrepreneur must pay attention to the application of the FAP. If his company registers a greater number of accidents or occupational illnesses, he will pay more. Now, if his enterprise does not get any case of work accident, he will have a bonus, which is a 50% reduction in the tax rate”, warns Jean Carlo.

THETax Lead Codeperforms the reclassification and recovery of RAT credits based on the aforementioned changes, which may generate excessive or mistaken payment by the company, according to the company's preponderant CNAE, by head office or branch. "We carry out the process administratively, for the immediate use of the credit that the company has, in addition to the possibility of considerably reducing the amount due for the contribution, and often the head office can fall under a CNAE 3%, for example, and the branches 1%, and in practice we see all employees being rated as 3%. The entire analysis takes into account the Normative Instruction (IN) 1453/14, which provides for the new framework for this calculation", explains the CEO

Enterprises that provide services through the assignment of labor or contract work must retain 11% of the gross value of the invoice, invoice or receipt for the aforementioned service provision and pay it to Social Security. Known as Retention of 11%, this contribution is also refundable, as long as the amounts have not been offset on the payroll. This accounting is provided for in IN 1300/12 and is also done on an administrative basis."In this case, the amounts paid in excess resulting from the difference between the retention of 11% and the billing together with the amount of social security contribution due on the payroll are considered. So the company needs to gather the documentation related to the amounts withheld, such as invoices, service provision contracts and accounting movements. The amount is credited to a checking account, corrected by SELIC"

Tax Review Tax at zero initial cost.

It is perceived that social security compliance can ensure the company complies with all rules and laws imposed for the segment in which it operates with zero initial investment. However, such calculations are thorough and require the presence of experts in the tax area for greater security. "THETax Lead Codeperforms all services under conservative standards, pacified by the Federal Revenue of Brazil. In other words, the entrepreneur will have the security of the data obtained. In addition, the taxpayer will only have costs in case of success and after obtaining economic or financial benefit, and for that, just look for one of our establishments to clarify doubts and start this verification”, concludes Jean Carlo.

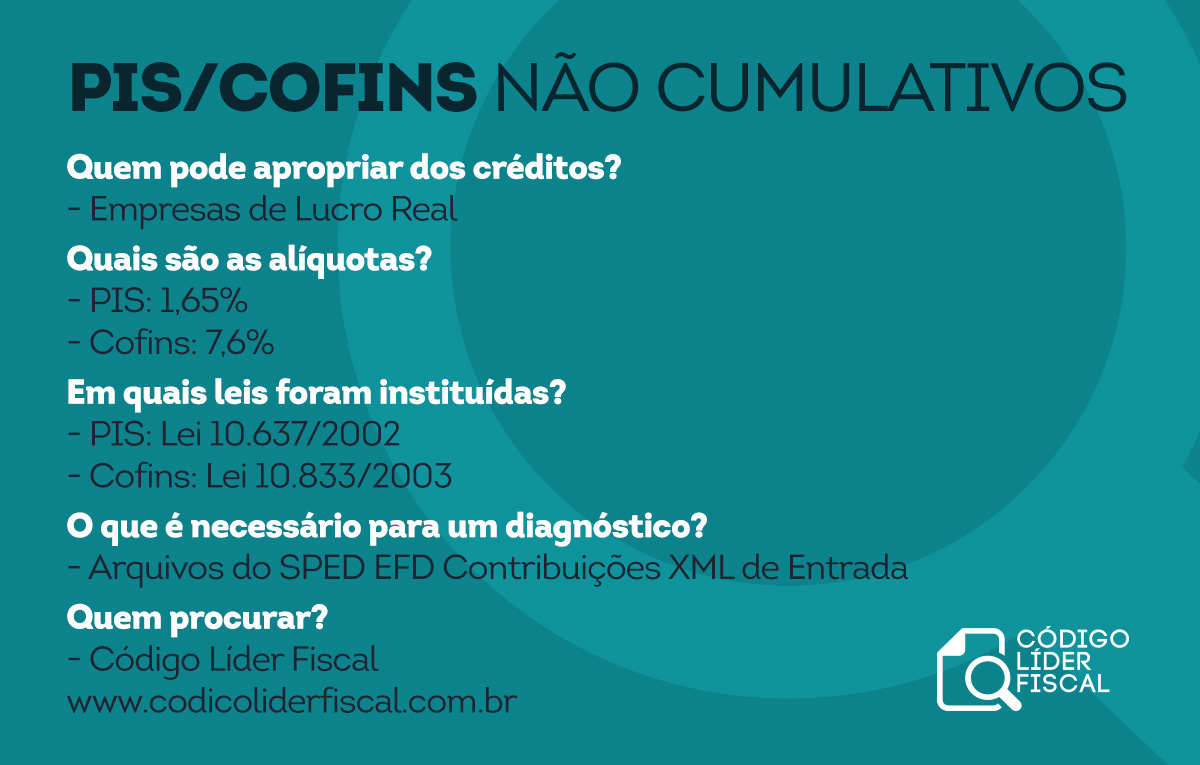

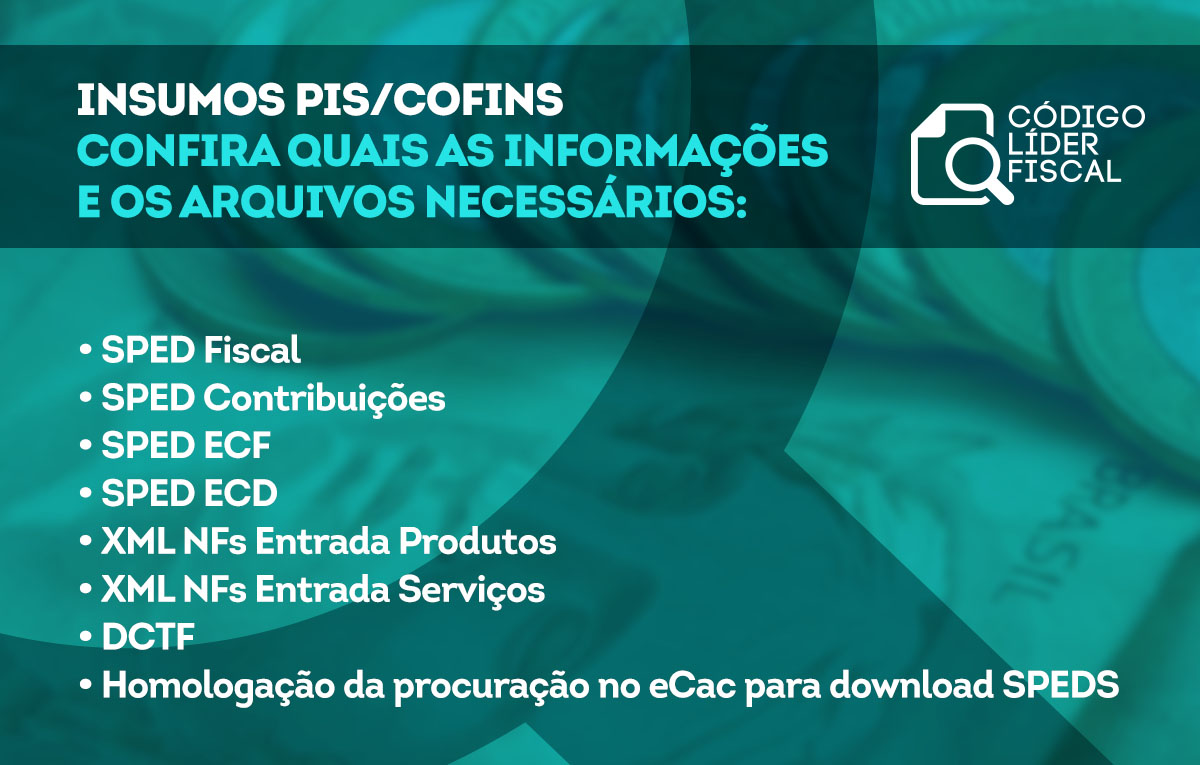

Laws 10.637 and 10.833/03 established the rules for the non-cumulativeness of PIS and COFINS. At rates different from those established in the cumulative regime, the calculation basis for these contributions considers the total gross revenue of the companies, less credits allowed by law. Thus, taxpayers opting for Taxable Income should pay attention to the accounting of the lower amount to be collected and seek the support of companies specialized in this tax review.

The Social Integration Program (PIS) and the Contribution to Social Security Financing (Cofins) are federal government taxes directed at legal entities. They are applied through two regimes: cumulative and non-cumulative. The first is provided for in Law 9,718/1998 and has rates of 0.65% and 3%, for PIS and Cofins, respectively, applied to the total gross revenue earned. In the non-cumulative regime, a little more recent, the PIS and Cofins rates were changed to 1.65% and 7.6%, respectively.

Non-cumulativeness allows that, when purchasing a product, the company has credit for the contributions that will be compensated in the sale of the product. "Taxable Profit companies have millions of items purchased monthly that generate PIS and COFINS credits and 99% of the time the full use by accounting becomes impossible due to the complexity of recording millions of Incoming Invoices, with thousands of NCMs and different rates and suppliers and ERPs, and numerous deadlines to meet, and in this scenario, the Codigo Lider Fiscal stands out with the review of NON-CUMULATIVE PIS and COFINS credits, through artificial intelligence, which generates debit reports and credits, at a distance and in about 30 working days”, points out the CEO of the Tax Leader Code, Jean Carlo Sene.

Among the items for possible appropriation of PIS and Cofins credits are, for example: goods or services purchased for resale or used as input, electricity; rents paid to legal entities, improvements, maintenance, fixed assets, intangible assets, returns, among others.

recent decisions

In April 2018, the Superior Court of Justice (STJ) determined that everything essential for the development of economic activity should be considered "input" and in December 2018 the Internal Revenue Service published the Cosit Normative Opinion 5/2018 which pacified the theme that gives credit to everything that is considered essential or relevant to the company's activity. The decision, which has already started to be applied by the Administrative Council of Tax Appeals (CARF), underlies the broad right of credit interpretation and, consequently, the preservation of non-cumulativeness.“Before this STJ decision, this concept of input was restricted by the Federal Revenue Service, expenses directly related to production, which caused countless losses to taxpayers. Now, there is the news that, if expenses are essential or relevant to the activities of companies, there must be credit”, explains CEO Jean Carlo.

Specialized company

The Tax Leader Code has parameterized in addition to the legislation that gives the right to PIS and COFINS credits, all possibilities exemplified in Normative Opinion 5/2018, as other Consultation Solutions and jurisprudence that support analogies that characterize the right to PIS and COFINS credit for activity of each company. “We are always based on the laws and solutions for consultation and decisions of the CARF, as well as judicial decisions. We work with a set of technologies that enable the crossing of digital files with company information to calculate the credits for these contributions”, concludes Jean Carlo.

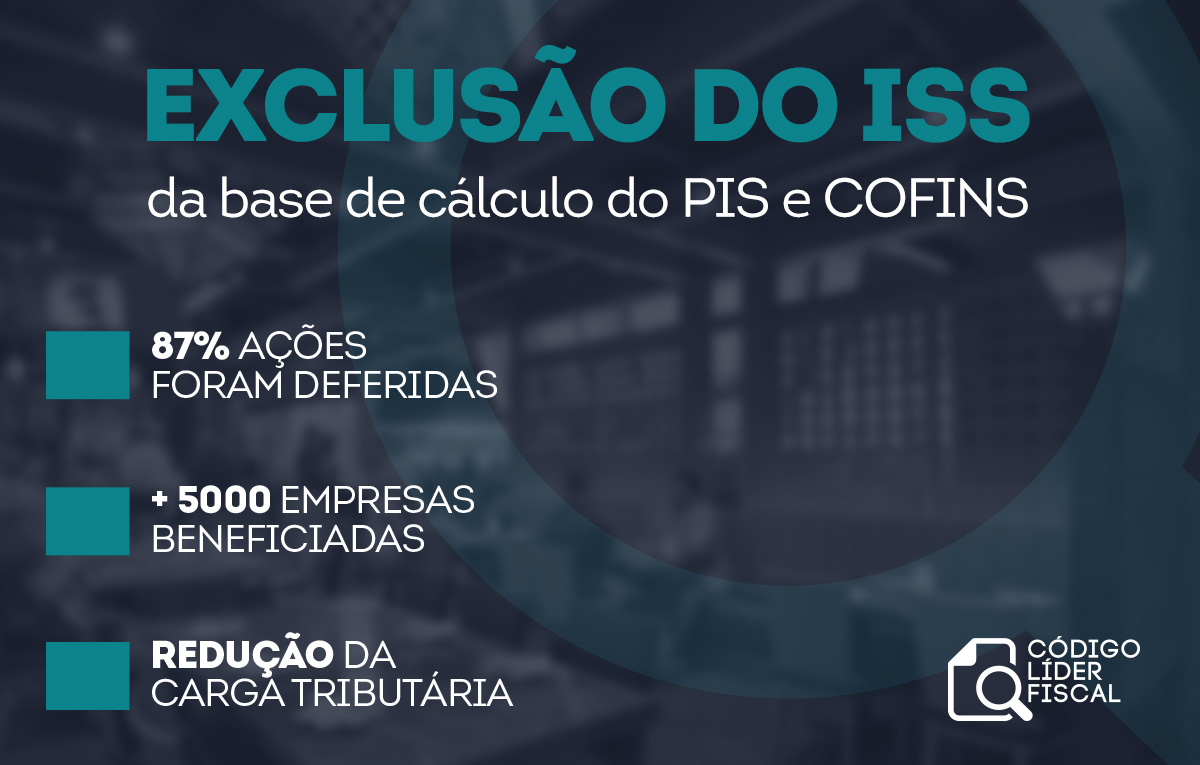

The Federal Supreme Court understands, by RE 592,616 of 2017, that the amounts as Service Tax (ISS) should not be included in the calculation basis of the Social Integration Program (PIS) and the Contribution for Social Security Financing (Cofins ). The reference for this understanding is in the res judicata of theICMS, at RE 574,706of the same year, with the defense that such amounts do not represent revenue. Beneficial for taxpayers, this decision makes it possible to offset amounts unduly collected in the last five years.

ISS is a municipal tax that is levied on companies and self-employed professionals, service providers. It covers segments of health, transportation, construction, information technology, among others. The rate must be checked by the taxpayer in the municipality in which it operates, but may vary according to the service provided, with a maximum of 5%. The company that does not pay the tax is irregular with the city hall and may suffer fines and interest.

The good news is that taxpayers will be able to exclude the tax amount when calculating PIS and Cofins contributions. The amount collected as ISS does not represent wealth or profit in the economic activity that the company carries out, only for the collecting body. “One must think of the same logic as the exclusion of ICMS. Even if the ISS is a tribute to municipal tax and the state ICMS, are similar in nature and, therefore, the Supreme Court meant for both the same rule and application, "explains the CEO of Code Tax Leader, Jean Carlo Sene

Still, entrepreneurs can request the recovery of amounts paid in excess in the last five years, prior to the process.“Through this judicial measure, we can determine and offset the credit for undue payments. This will certainly have a positive impact on the companies' cash flow, both by reducing the tax burden and by recovering the aforementioned amounts", praises the CEO

Featured in tax advice

More than five thousand companies have already benefited from actions related to the exclusion of ISS from the PIS and Cofins calculation basis. In all, 87% of the processes initiated by theTax Lead Codethey were aproved. “We work with the security of having a specialized team and using state-of-the-art technology, capable of reading 60 thousand lines per second. We offer the entrepreneur the possibility of joining this legal discussion, among others such as the exclusion of PIS and COFINS from their own contribution base, at zero cost, with remuneration only after the final decision and the peace of mind of being up to date with the tax obligations that regulatory bodies require. All of this, enabling him not to bear undue amounts, often necessary for the company's survival”, concludes Jean Carlo.

The exclusion of the Tax on Circulation of Goods and Services (ICMS) from the calculation basis of the Social Integration Program (PIS) and the Contribution to Social Security Financing (Cofins) is favorable to taxpayers. Even recent, the decision is still subject to many doubts and requires great caution from the entrepreneur. To save on tax collection and recover amounts paid unduly, companies must prepare for this accounting.

The decision of the Federal Supreme Court, through RE nº 574.706, states that ICMS should not be considered as revenue and, therefore, should not serve as a basis for calculating PIS and Cofins. As a result, real profit and presumed profit companies are entitled to contribution credits, calculated on the exclusion of this tax. “The unconstitutionality of excluding ICMS from the accounting of these contributions has been discussed for over 20 years. And recently the decision favored the taxpayer, understanding that once paid by the company, the ICM does not return as equity, thus it should not be collected”, explains the CEO of the Tax Leader Code, Jean Carlo Sene.

Taxpayers still need to pay attention to other factors related to PIS and Cofins credits. There are several aspects that must be observed, as explained by Jean Carlo. "The main traps that the entrepreneur must take into account are the legal rules, as a method of calculation, and the different forms of incidence of PIS and Cofins on each type of product sold, such as those taxed, at a zero rate, or with thesingle-phase taxation regime, ICMS ST, among others".

Another difficulty that taxpayers may face is gathering all the documentation, taking into account processes that have been in process for more than 15 years. The CEO also reinforces that an incorrect quantification of values can cause many problems for companies. "The right time for the accounting recognition of this asset must be observed and caution must be exercised in carrying out the calculation of credits. Otherwise, the taxpayer may be subject to restrictions imposed by the tax authorities, ranging from notifications of payment to the drawing up of infraction notices and imposition of fines”, he points out.

Repercussions of the decision Since the decision of the Supreme Court, which ended years of analysis of the subject, taxpayers still find an imprecision: which revenue should be taken into account when processing this data. The collected or highlighted in invoices? According to the STF's position on RE, which was also later reinforced by Minister Gilmar Mendes, the calculation of the exclusion of ICMS from the PIS and Cofins base must consider the entirety of the tax highlighted in the invoices, that is, its gross revenue. What can confuse the taxpayer is the internal consultation solution No. 13/2018 published by the Federal Revenue, which must be considered the net value of ICMS to be excluded from the calculation basis of contributions, that is, the amount owed by the company. According to the CEO of the Tax Leader Code, Jean Carlo de Sene Sousa, the position to be followed is that of the STF. “We carry out data processing in accordance with the Supreme Court decision, which is good news for companies. It is this decision that really pays them the correct amount back”, he says.

Search for specialized companies These and other inaccuracies that run through the fiscal and tax sector can make the company bear undue amounts, whether with payments made higher or lower than those established by regulatory agencies. To avoid fiscal problems and correctly monitor the inconsistencies of the area, it is always advisable to look for aspecialized companiesin these accountings.

“The tax area is delicate and requires great caution from businessmen. Therefore, having companies specialized in the field to deal with specifics like this and with the necessary tax knowledge is extremely important, both for the security of a business and for the tranquility of an assertive accounting within what is governed by current legislation. THETax Lead Code offers a free diagnosis for several services in the tax area with the aid of artificial intelligence, a technology capable of reading 60 thousand lines per second”, he concludes.

Credit: Graphic creation / Felipe Ramos

The Tax Tax Review can be decisive for the regularity of the company before the tax authorities.

Keeping up with tax contributions is a challenge for entrepreneurs. The insecurity of dealing with the constant changes in the Brazilian tax system leads many taxpayers not to pay taxes properly. A survey carried out by the Brazilian Institute of Tax Planning (IBPT) indicates default in 27% of large companies, 49% of medium and 65% of small ones. A reality that can be changed with the help of companies specialized in the area, which offer solutions to the taxpayer through financial planning tools and a more predictable fiscal scenario.

Taxes owed by companies can be collected in two ways: by tax notification, such as IPTU and IPVA, and by registration, monitoring and accounting by the taxpayer, such as PIS, Cofins, ICMS, among others. "And it is in this opinion that, many times, the entrepreneur becomes irregular before the inspection bodies, either due to default or, in more serious cases, tax evasion. There are numerous rules to be observed and applied for specific profiles of each company. Therefore, having a Tax Tax Review, annually, through the processing and crossing of tax files SPEDS and NFs, combined with artificial intelligence, and the help of qualified professionals prepared for the calculation is of paramount importance", points out the CEO of Leading Tax Code, Jean Carlo Sene.

Also according to the CEO, inspection is increasingly strict, with the implementation of effective technologies and techniques, capable of easily identifying irregularities in companies. "What an entrepreneur should keep in mind is that the tax review is beneficial and does not mean greater expenses for the company, on the contrary, it is the main means of ensuring regularity before the tax authorities and the possibility of discovering, by legal means, the collection the largest of taxes, obtaining an ideal cash flow for the operation of the business”, he warns.

Among the main administrative reviews, through technology, are theSocial Security Compliance, and the non-cumulativeness of PIS and Cofins, which promote the issuance of an accurate diagnosis and help in recovering amounts paid unduly. "We will identify whether the calculation basis of theSEFIPis not at odds with the FOPAG basis; if there are no amounts of indemnity character suffering incidence of INSS; if theRAT and FAPhave been reclassified annually; and if the PIS and Cofins credits were not used in accordance with Laws 10.6737/02 and 10.833/03, the recent decision of the STJ and the Normative Opinion No. 5 of the Federal Revenue, which expanded the concept of inputs, enabling the taking of credits from items considered essential or relevant to the activity of the Taxable Income companies, in the non-cumulative regime”, explains Jean Carlo.

The CEO reinforces that, even with the complexity of the Brazilian tax system, tax obligations must be up to date. “When we deal with an area as detailed as tax, the ideal is to have professionals who understand the subject at our side. AtTax Lead CodeWe have specialists who aim to provide taxpayers with the security and tranquility of assertive accounting, avoiding both tax evasion and overpayments. Furthermore, the client will have the necessary tax and legal assistance so that the Tax Tax Review is based on current regulations and laws”.

Tax Review Tax at zero initial cost

It is noticed that the Tax Tax Review can ensure the company compliance with all the rules and laws imposed for the segment in which it operates, with zero initial investment. “The Tax Leader Code performs all services under conservative standards, pacified by the Federal Revenue of Brazil. In other words, the entrepreneur will have the security of the data obtained. In addition, the taxpayer will only have costs in case of success and after obtaining economic or financial benefit. To do this, all you have to do is look for one of our establishments, ask questions and start checking”, concludes Jean Carlo.

Credit: Graphic creation / Felipe Ramos

The fiscal and tax review must be carried out with the help of specialized companies and trained professionals.

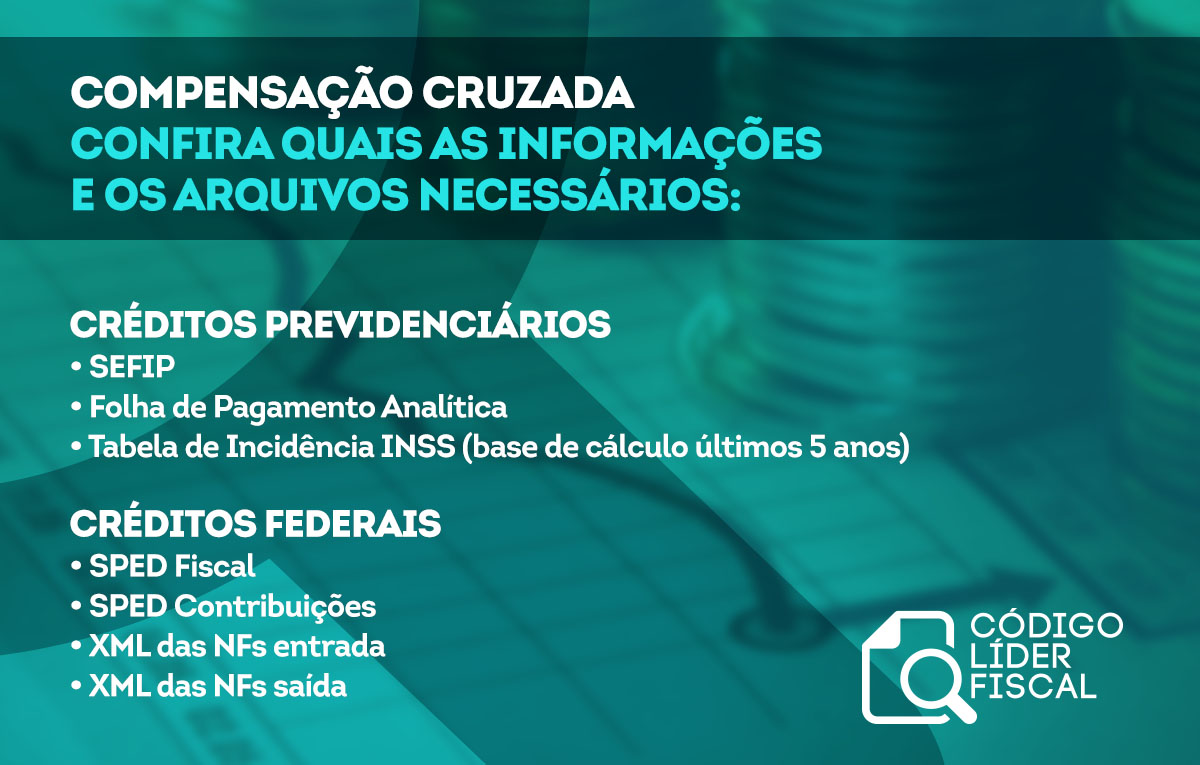

The Normative Instruction No. 1810 of the Brazilian Federal Revenue regulates the unification of tax compensation regimes for legal entities that use the Digital Bookkeeping System for Tax, Social Security and Labor Obligations (eSocial). Through cross or unified tax compensation, companies that have social security (INSS) and treasury (PIS, Cofins, IRPJ, CSLL, etc.) credits before the Federal Government will be able to calculate the social contributions due and offset debts, subject to restitution or reimbursement.

The decision was in line with an old demand from taxpayers. With the change, implemented in Law No. 13.670/2018, social security credits and debts may be offset, by means of a Declaration of Compensation (DCOMP), with any federal taxes, subject to the appropriate restrictions imposed by legislation arising from the transition between the regimes.

The update does not allow the cross-compensation of debts calculated in periods prior to the use of eSocial. “This standard is linked not only to the implementation of eSocial, but also to the Declaration of Federal Tax Debts and Credits (DCTF) Web, which replaces the use of SEFIP/GFIP. As for taxpayers who do not use eSocial, the procedure remains unchanged, that is, the compensation regime through information in GFIP does not change”, explains the CEO of the Tax Leader Code, Jean Carlo Sene.

With a positive impact on the company's cash flow, the benefit becomes an important economic planning tool. "The taxpayer will not have the cost to pay the tax due, and it is possible to use credits for this process in a faster and more organized way, without the need to wait months for the refund request with the Revenue. Then, the follow-up of credits and the opening of administrative processes and procedures will be facilitated, which allows the tax authorities to better identify infringements”, he adds.

The deadline for requesting compensation or refund of taxes is five years, considering the correction of the Selic rate due. “For the request in cases of cross compensation, the data transmitted by DCTFWeb will be used, that is, they will be more restricted to the moment when the company effectively joined e-Social and started transmitting it through this declaration. A complete diagnosis must be made, with a survey of contributions paid in duplicate, all to grant the right to credit”, points out Jean Carlo.

The CEO advises that maintaining the fiscal and tax review is a factor of great importance for the company to enjoy the benefit and avoid irregularities before the tax authorities. “We are dealing with a refund that needs professional monitoring to avoid the risk of inconsistent information. The company will need the assistance of adequate systems and strategies for this compensation. AtTax Lead CodeEffective tools and artificial intelligence are used to provide the taxpayer with data security and consistency throughout the process. We promote the survey of recovery opportunities, review the rates and calculation bases, and identify any divergences and necessary corrections. Furthermore, we enable an initial diagnosis at zero cost, in which the taxpayer will only pay when, and if, it is successful", concludes the CEO

Credit: Graphic creation / Felipe Ramos

The Tax Leader Code has state-of-the-art technologies and a specialized team capable of calculating

The absence of a constitutional definition of the term “input”, presented in laws 10.637/2002 and 10.833/2003, for PIS and Cofins, respectively, in the non-cumulative regime, is the cause of numerous discussions in the field of Tax Law. Controversial topic, debated for over 15 years, received, in December 2018, a normative opinion, Cosit 5, from the Federal Revenue of Brazil. The intention of the document is to put into practice criteria previously established by the Superior Court of Justice (STJ), and guide the inspection, compensation and compensation procedures that involve the matter.

The STJ's definition, made at the beginning of the same year, considers as input everything that is essential or relevant to the company's economic activity. “This position placed as illegal two Normative Instructions, 247/2002 and 404/2004, from the Revenue itself, which applied and defended to PIS and Cofins the concept of input as similar to that used in the IPI. Something that is not consistent, considering that the IPI is levied on the output of industrialized products and the PIS and Cofins on the total revenue earned", contextualizes the C.E.O of the Tax Leader Code, Jean Carlo Sene.

The STJ statement expanded the concept of input and, consequently, the limits for crediting contributions, which gave the concept an opening to subjectivity. “Cosit 5 analyzes the positioning of the STJ and places the definition of inputs within the criteria of essentiality. This implies as an input concept, then, everything that is intrinsically necessary for the production of goods intended for sale or for the provision of services by the legal entity. In other words, only the fundamental items for the production of the good or service are inputs”, clarifies the C.E.O.

The opinion brings positive points to taxpayers, such as the expansion of possibilities for using credits from PIS/Cofins contributions. Items subject to credit are considered, for example: Personal Protective Equipment (PPE), in industries, and vaccines applied to herds, in the case of rural producers. "This opinion effectively gives an understanding of the credit limits for companies and, mainly, it recognizes the right to credit in the so-called 'input of inputs', that is, in the use of inputs for the manufacture of input good in the production of intended good for sale or in the provision of services to third parties”, he continues.

"For the correct calculation of the reimbursements to be received, it is necessary to review all the calculations of credits related to the last five years so that the amounts that can be used with the new understanding of the Revenue are raised. Also, the identification of opportunities to reduce the tax burden through the correct calculation of credits.”

The C.E.O warns that this accounting will require an increasingly specific treatment on the part of taxpayers, therefore, relying on the help of trained professionals for this calculation is essential. "The Tax Leader code performs the accounting of this collection using Artificial Intelligence and Machine Learning, capable of reading 60 thousand lines per second. In addition, with the expertise of a team prepared and updated with current regulations and laws. All of this allows for a deeper and more consistent analysis that effectively promotes the financial return to the taxpayer”, concludes Jean Carlo.

Simples Nacional is a system that simplifies the payment of taxes for companies with annual gross revenue of up to R$4.8 million. Data from DataSebrae show that more than 11 million companies opt for this regime, an increase of 64% between 2012 and 2016. There is, however, a lack of knowledge about this tax system that can make the entrepreneur bear amounts above those required by law. For the correct accounting of overpaid taxes, taxpayers should look for professionals in the tax area.

Provided for in Complementary Law No. 123, of 2006, the Simples Nacional (SN) aims to facilitate the accounting and tax situation of entrepreneurs of micro and small companies. Before this legislation, small businesses paid federal, state and municipal taxes, through separate guides, without distinction from large corporations. With SN, payment is made in a single tab, called DAS. The problem with this taxation lies in the tax calculation basis that is made on the sales revenue earned each month. Therefore, companies that sell products subject to the Tax Replacement of ICMS (ICMS-ST) and PIS/Cofins single-phase regime will have double payments .

The problem with this taxation lies in the tax calculation basis that is made on the sales revenue earned each month. Therefore, companies that sell products subject to the Tax Replacement of ICMS (ICMS-ST) and PIS/Cofins single-phase regime will have double payments .

To minimize this issue, Complementary Law No. 147, of 2014, determined that sales of products in the tax and single-phase substitution regimes were excluded from the ICMS and PIS/Cofins calculation basis, respectively. “That's why it's extreme importance of a professional and specialized service for this tax review. The procedures and accounting for this tax require a lot of knowledge" warns the Chief Tax Officer of the Tax Leader Code, Jean Carlo Sene.

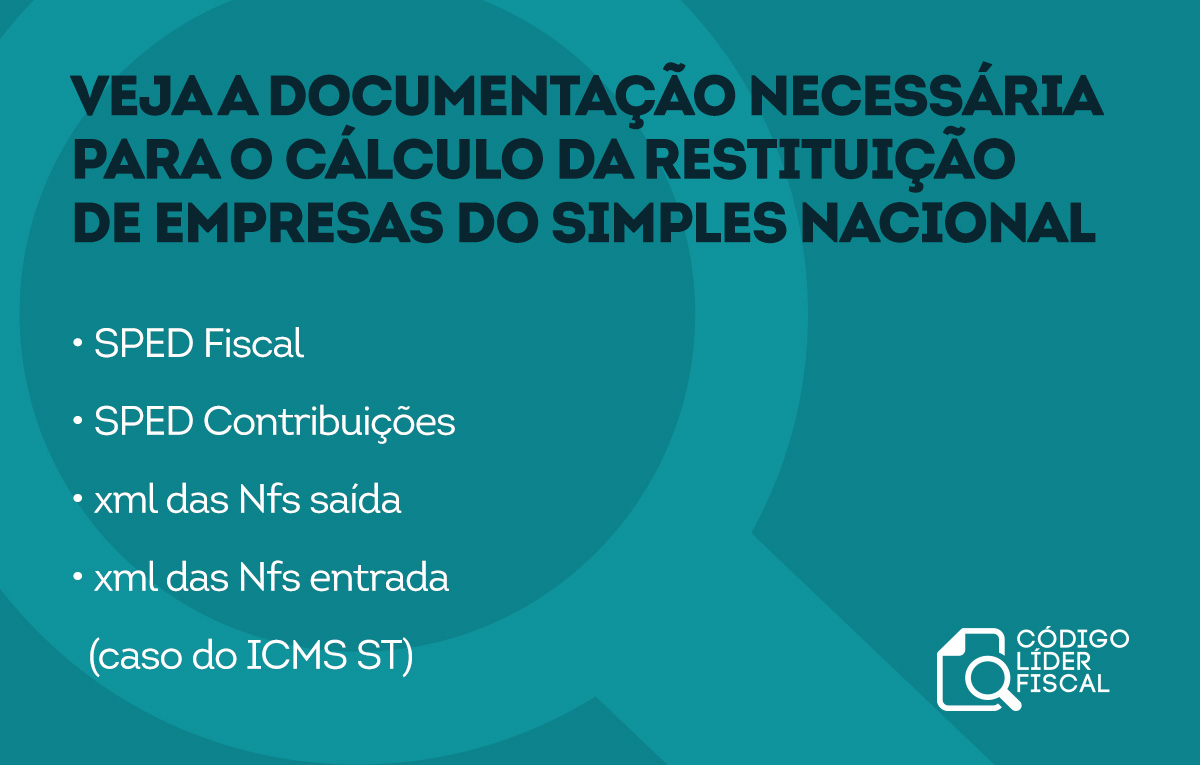

A model for offsetting overpaid taxes in a five-year retroactive period is made available by the Internal Revenue Service. “When looking for one of our professionals, the taxpayer will receive guidance on what documentation and data are needed for this recovery. It serves as an alert to the importance of the company's document and fiscal organization for the agility of this process”, adds Jean Carlo.

Also according to the CEO for this work, specific software and tax specialists are needed, as provided by the Tax Leader Code. "It is possible to identify 100% of these single-phase and ST revenues with the crossing of NCM codes sold and the invoices of output of the last 60 months. Also, make the rectification of the PGDAS and the refund request administratively. Best of all, the Internal Revenue Service refunds these taxes in the current account, usually within 60 days", he concludes.

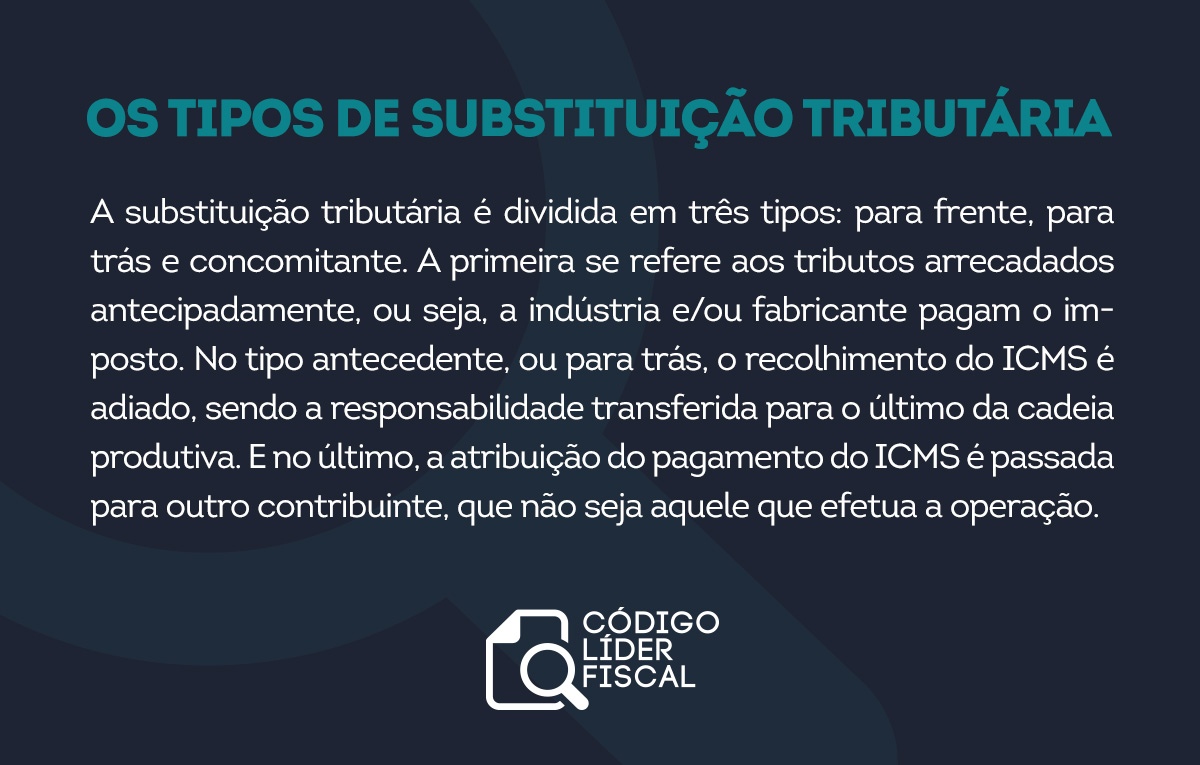

Tax Substitution (ST) is one of the ways to collect taxes in Brazil. Provided for in the Federal Constitution, article 150, aims to facilitate inspection. For it, the responsibility for paying ICMS is assigned to another taxpayer and charged only once. The ST is used by federal and state governments to collect the Tax on Circulation of Goods and Services (ICMS) and can generate considerable savings in a company's cash flow, if the rules and reimbursement opportunities are observed.

In practice, a company is responsible for paying the ICMS-ST due throughout the production chain. In general, the concentration is made in industries and importers. “With tax substitution, the tax authorities do not need to supervise everyone in a production chain, such as retailers and wholesalers, they will only monitor manufacturers and importers, who are solely responsible for paying the tax. It is an anticipated collection, as the government does not need to wait for the final sale of the merchandise to receive it”, explains the Chief Executive Officer of the Tax Leader Code, Jean Carlo Sene.

Among the most common products in this collection are: fuels and lubricants, beverages, cigarettes, cleaning and construction materials, medicines, food products, among others defined in regulations of the National Council for Finance Policy (Confaz). “We have a more common type of TS, which is forward. That is, a soft drink manufacturer, for example, pays the tax in full and, consequently, relieves wholesalers of having to worry about calculating the tax, whether when buying or selling this product"

There is no increase in the tax burden in the application of this regime, much less negative impacts for the final consumer. “In theory, this collection corrects irregularities, one of which is the reduction in tax evasion. In general, the final price of the product is already suggested by the manufacturer or importer for retail sale, that is, it reduces dishonest competition and increases the company's administrative efficiency, since the tax was collected in advance and it will not need to worry about yet another tax bureaucracy, but in practice it harms the entrepreneur who, in most cases, resells the same products at a lower value than that which was taxed in advance”, he adds.

The C.E.O Jean Carlo alerts to the specificities of each State in the application of the ST. “The Tax Replacement Specifier Code (CEST) was created to separate products that have or do not have ICMS-ST. But the fact that a product is in the table does not mean that it is automatically subject to tax substitution. Each state has specific products. So, in addition to being in the CEST, the merchandise must also be regulated by the State for this collection”, he points out.

The Tax Replacement Regime also allows for the recovery of amounts paid in excess. “It is very important that the entrepreneur is aware of all the obligations and benefits he has under the tax rules. Therefore, it is advisable that he seek professional help. In the Tax Lead Code We provide the diagnosis free of charge, through the signing of a successful contract, where there will only be costs to the entrepreneur after the economic or financial benefit. We have effective technologies capable of promoting the taxpayer's financial return. All with the security and tranquility of a job based on the laws in force”, concludes C.E.O Jean Carlo.

The Brazilian tax system undergoes constant changes, so being aware of economic transformations and regulating tax obligations is a huge challenge for the taxpayer. According to data from the Brazilian Institute of Planning and Taxation (IBPT), every day, an average of 30 new rules are published in the country. The survey also states that companies spend, on average, 1958 hours annually for the management and payment of mandatory taxes and need to follow more than 3700 rules per year.

To save this time and have a safe and assertive accounting, the use of new technologies, such as artificial intelligence and robotics, is of great value.“Our country has a complex tax payment system that is associated with state and federal taxes. So, like any other area, the use of technology in the tax sector is important for a safe, more agile work, based on tax updates, as it can foresee the constant changes in this scenario", explains the CEO of the Tax Leader Code, Jean Carlo Sene.

Specialized software is used to automate the work and issuing of payments."When we talk about security, we mainly refer to the tranquility that the taxpayer will have that everything that is mandatory will be fulfilled on time, the amounts will be collected correctly, without overpayments, generating savings for the company, and without the possibility of tax evasion fraud”, he continues.

Even with all the technology already present in the tax area, the presence of a professional prepared to analyze the materials and conduct the software is essential. “Artificial intelligence makes it possible to support a greater volume of data and analyze all the information necessary to comply with tax obligations, but without a team prepared for this assessment, the taxpayer will continue with the same problems”, he points out.

Also according to C.E.O Jean Carlo, technology companies specialized in such data processing have the expertise of all the legislation of the current tax system. “The use of technology in favor of the entrepreneur in the correct calculation and identification of taxes is viable not only to guarantee greater precision and speed, but also a more peaceful sleep. Therefore, the search for this help from professionals, together with the artificial intelligence technology that the area already allows, is an essential factor when we understand that the best defense for tax inspection today is to face that the dispute will only be fair when the battle it is machine against machine, or T-Rex against T-Rex”, he praises.

The Tax Leader Code is a national company, headquartered in Belo Horizonte and offices in 4 other states, the Tax Leader Code uses artificial intelligence and technology capable of reading 60 thousand lines per second. “We identified the amount that the taxpayer is entitled to recover from taxes improperly paid in the last five years. We offer tax and fiscal solutions in the speed and security that the taxpayer needs” points out C.E.O Jean Carlo.

Currently, the Tax Leader Code is the only company in the country to deliver to the entrepreneur a thorough analysis of 100% of the items recorded in Speds and purchase and sale invoices. “We issue reports in about 40 days to be used immediately with the crosses considered liquid and certain. We increased the profit margin and reduced the tax burden, all through a technology that helps in the validation, processing and crossing of data and information”, he concludes.

Credit: Graphic creation / Felipe Ramos

Exclusion of tariffs could result in a material economic impact for the company.

With relevant social scope, the exclusion of the Tariff for the Use of the Transmission System (TUST) and the Tariff for the Use of the Distribution System (TUSD) from the calculation basis of the Tax on Circulation of Goods and Services (ICMS) is one of the major discussions of the Brazilian Judiciary. Still subject to future positions, the illegality presented, and already under discussion by the Superior Court of Justice, is favorable to taxpayers and allows the reimbursement of payments made in excess in the last five years.

Electricity is used by most Brazilians, reaching more than 80 million consumers. Therefore, understanding the composition of the energy bill and the types of actions that can be taken on it to generate savings in companies is essential. “From the moment when energy is generated until it arrives at the consumer, we have tariffs that must be analyzed. They are transmission and distribution. The first, TUST, refers to the line traveled by electricity from the generating plant to the substation. The TUSD, on the other hand, is the distribution network from the substation to the home or business, that is, to the final consumer”, explains the C.E.O of the Tax Leader Code, Jean Carlo Sene.

Irregular ICMS calculation on TUST and TUSD can result in a relevant economic impact, with an increase of up to 10% in the final value of the electricity bill. “The thought is that both TUST and TUSD and sector charges are not services provided to the consumer, they should not be equivalent to a commodity. Therefore, it would be correct to charge only the Energy Tariff, which is effectively consumed by the taxpayer. Only it, then, could be levied on the ICMS rate”, he continues.

Based on divergent decisions and still subject to several discussions, the exclusion of tariffs should be part of the company's financial planning and analyzed by professionals specialized in the subject, with the security of negotiations in a predictable and current scenario. “At Tax Leader Code we are protected from the safety of a work guided by the laws and regulations in force, always with the help of state-of-the-art technology, such as artificial intelligence, and with the participation and legal support in all parts of the process”, points out Jean Carlo.

The C.E.O further explains that calculations like this can generate a positive cash flow for the taxpayer and ad aeternum monthly savings. “We identify the installments, make the correct calculation of the refund for the last five years and submit them to the Judiciary Branch for analysis. It is important to emphasize that the Tax Lead Code carries out the tax review at zero initial cost and there will only be successful remuneration if, after the final decision, the decision is favorable to the taxpayer”, he concludes.